To open a free business checking account online with no deposit is one of the easiest ways to start managing your business finances efficiently. This kind of account is usually opened for small business owners and freelancers. To qualify for this kind of account, you should be a sole proprietor, single-member LLC, partnership, or corporation in the United States.

To open a free business account, you must provide basic identity and business documents. If we open this kind of account, the benefits include no upfront cash needed and faster online setup. You also get lower monthly costs and easy integration with accounting and payment platforms.

Here, I compare the best online business checking accounts from banks and fintechs. I explain the application process and list the documents you need, like an EIN or Articles of Organization. I use FDIC guidance and resources from NerdWallet and Bankrate to ensure accuracy.While this guide focuses on the United States, it’s important to note that banking regulations, identification requirements, and business structures vary significantly from country to country also may be the procedure for opening a business account elsewhere may differ, but this guide provides a solid understanding of the overall process.

Essential Considerations before Opening an Account

- Anyone who has right ID and business paperwork can open a free online business checking account with no deposit easily.

- Sole proprietors and single-member LLCs face the simplest verification; corporations need more documentation.

- Compare fees, transaction limits, and mobile deposit rules when choosing the best online business checking account.

- FDIC insurance, bank disclosures, and resources like NerdWallet and Bankrate are key references I use.

- Watch for differences between “no deposit” and banks that require an initial ACH or in-person funding to fully activate the account.

Benefits of Opening a Free Online Business Checking Account

More business owners are choosing digital banking. New payment systems and mobile tools make online accounts great for small teams and solo owners.

Online banks offer low costs and quick access to payment tools. This attracts freelancers and small businesses. You can open an account from your phone and start accepting payments without going to a bank.

Benefits of zero initial deposit accounts for startups and side gigs

New businesses and side hustles can keep personal and business money separate without using up cash. Zero deposit accounts make it easy to start. These accounts let you start accepting payments right away. You also get a business debit card for expenses. This helps manage money during the early stages of growth.

Eligibility & basic requirements for business checking accounts

Most banks accept sole proprietors, LLCs, partnerships, and corporations. But some have special rules for certain industries or nonprofits, so it’s a good idea to check their requirements before you apply.

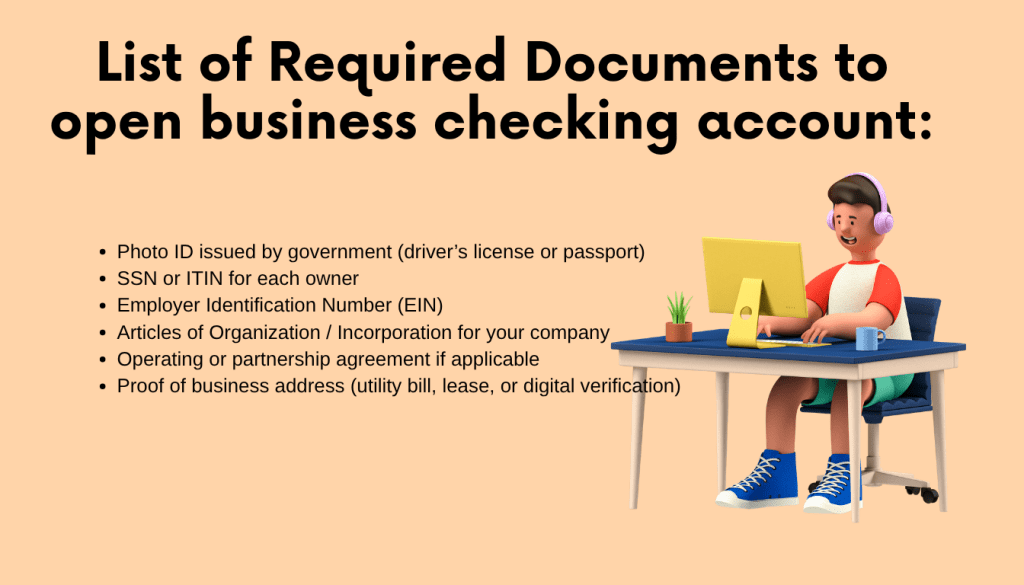

List of Required Documents to open business checking account:

- Photo ID issued by government (driver’s license or passport)

- SSN or ITIN for each owner

- Employer Identification Number (EIN)

- Articles of Organization / Incorporation for your company

- Operating or partnership agreement if applicable

- Proof of business address (utility bill, lease, or digital verification)

You may also need to confirm business ownership and sign consent forms. Being prepared makes it easier to finish the online application and avoid delays.

How to find banks and fintechs that explicitly allow opening with no deposit

I picked providers based on reputation and insurance status. I also looked for clear language on waivers. For neobanks, I checked app descriptions and onboarding screens. For traditional banks, I scanned account disclosures and branch policies.

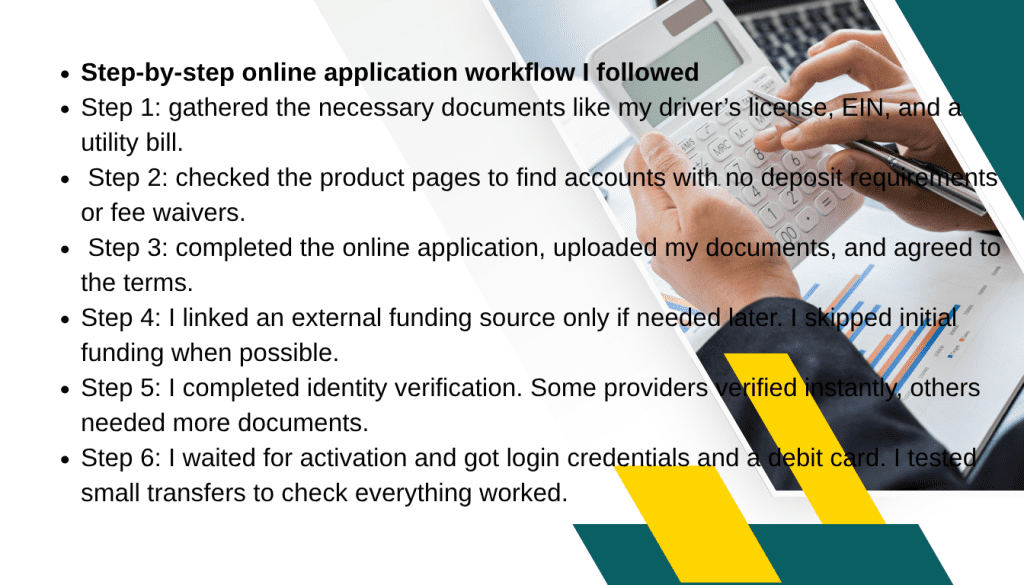

Step-by-step online application workflow I followed

Step 1: gathered the necessary documents like my driver’s license, EIN, and a utility bill.

Step 2: checked the product pages to find accounts with no deposit requirements or fee waivers.

Step 3: completed the online application, uploaded my documents, and agreed to the terms.

Step 4: I linked an external funding source only if needed later. I skipped initial funding when possible.

Step 5: I completed identity verification. Some providers verified instantly, others needed more documents.

Step 6: I waited for activation and got login credentials and a debit card. I tested small transfers to check everything worked.

Instant approval vs. delayed verification: what to expect

Many fintechs offer instant account approval and debit card access. You might face limits on ACH and daily transfers until verification is complete. Traditional banks do deeper reviews. This can delay full access while they verify your EIN, formation documents, and identity. This can take days to weeks.

Top Banks and Fintechs With Free Business Checking and No Deposit

I searched for the best options for small businesses and freelancers—reliable accounts that can be opened online with no deposit.Traditional banks like TD Bank offer online sign-ups for Business Simple Checking with no minimum deposit. Read agreements to understand ACH limits, reversal risks, and fees.

Fintechs and neobanks such as Novo and BlueVine often provide free checking with no balance rules, modern apps, and free ACH transfers. They are ideal for digital-first businesses, though cash deposits may have limits.

How to Choose the Best Online Business Checking Account

Always consider what your business really needs like as cash deposits, invoicing tools, or connections with QuickBooks or Stripe. If your business handles cash, choose banks with strong branch networks like TD Bank. For online freelancers, fintechs with free ACH and high mobile deposit limits work best.

Online Business Checking Account Comparison: Fees, Limits, and Features

I compare accounts by fees, limits, and useful features. Small pricing differences can affect real-world costs and convenience. I focus on payroll, vendor payments, and card use.

No Monthly Maintenance Fee vs. Waive Conditions

Many providers advertise no monthly fees. Some truly charge none, while others waive fees only if you meet balance or deposit requirements, or link another product. A no-minimum-deposit account might still need a $10,000 balance to avoid fees. Always read the fine print—“no fee” often comes with conditions.

Transaction Limits, Cash Deposit Policies, and Fees

Banks and fintechs use tiered plans with transaction and cash deposit limits. Basic plans may include 25–100 transactions monthly; higher tiers offer unlimited ones. Cash deposit limits vary from $6,000 to $30,000 per month. Exceeding limits can trigger fees around $2.60 per $1,000.

ATM Surcharge Policies and Out-of-Network Fees

Non-bank ATMs usually charge extra fees. Traditional banks only cover a few of these, but many fintech banks refund ATM fees up to a certain limit. Check ATM access where you operate. Reimbursement and international fees differ and can add up for frequent withdrawals.

Free ACH Transfers, Mobile Deposit Limits, and Debit Card Benefits

Many online accounts offer free ACH transfers, reducing payroll and vendor costs. I confirm if same-day ACH has extra fees.

How to Choose the Best Online Business Checking Account for Your Business

Start by thinking about what your business really needs—like cash deposits, invoicing options, or links to QuickBooks or Stripe. Choosing the right features now can save you time and money later.

Matching Account Features to Business Needs

If your business handles cash, choose banks with strong cash services like TD Bank.

For digital-first businesses or freelancers, fintechs with free ACH and high mobile deposit limits are ideal.

Evaluating Limits and Fee Schedules

Always read the fee guide before signing up. Look for details like monthly fees, transaction limits, and cash deposit charges. Sometimes paying a small fee is worth it if it includes free ACH transfers and more transactions. I also check ATM and cash-handling fees to make sure I’m getting the best deal.

Security, FDIC Insurance, and Protections

Ensure the account is FDIC insured or offers similar protection. Check for encryption, multi-factor authentication, and fraud safeguards—especially for LLCs.

For payment-processing businesses, verify how fast funds become available. Some accounts post next-day, which improves cash flow.

Final Recommendation

I weigh the cost of a no-fee account against one with more features. For most small businesses, a no-fee account is best if it offers solid features and strong security.

Step-by-step online application process and tips to speed approval

I guide you through a quick online application to get approvals fast. I share what I did to avoid delays. This makes opening a free online business bank account easy and fast.

Preparing a checklist of documents before you apply

I got everything ready before starting. I had a government ID, SSN or ITIN, and an EIN if needed. I also had Articles of Organization and other important documents.

I saved a business address proof like a lease or utility bill. Clear, high-quality scans saved time when banks asked for them.

Completing identity verification and business formation inputs accurately

I typed the legal business name correctly. Small mistakes cause manual reviews. I listed each beneficial owner and used SSNs as on government forms.

Many fintechs use instant ID checks and accept phone camera images. Traditional banks might need manual reviews and notarized copies. I uploaded clear files and matched dates and addresses to avoid extra checks.

How to handle requests for additional documentation or verification

If a bank asked for more, I replied fast with complete files. I didn’t upload partial files that cause questions. For proof of revenue or address, I sent bank statements or an invoice sample.

I kept copies of all documents and tracked my application. If updates were slow, I contacted customer support. This helped me open a free business checking account online with no deposit at several places.

Common pitfalls and how to avoid account restrictions or unexpected fees

I faced challenges when opening business accounts online. Small print on websites can hide big fees or limits. Always read the fine print and confirm steps before funding.

Some banks say you can open accounts with no deposit. But, this usually means no opening deposit, not no steps to start. You might need to link an account or make a small transfer first. Check if the account really lets you open without deposit and what’s disabled until you fund or verify.

Maintaining fee waivers and daily balance rules.

No minimum balance checking seems great for startups. But, fee waivers often require a minimum balance every day. If you miss a day, you could face the full fee. Make sure you understand the balance rules to avoid fees.

Risks with early availability of ACH funds and reversals.

Early ACH access can be helpful. But, services like TD Early Pay can be risky. Banks might reverse funds if the sender cancels or returns the payment. Keep extra money in accounts with early access to avoid overdrafts and reversal fees.

To avoid surprises, I check a few things before committing. I make sure the account lets me open without deposit. I also check the balance rules and early access programs. This helps me avoid holds, reversals, and unexpected fees.

Conclusion

Choosing the right online business checking account is important. I looked at fee guides and bank rules carefully. This included checking ACH policies and early availability rules from banks like TD Bank. Make sure the account really has no deposit, is insured by FDIC, and fits your business needs.

Some tips helped me a lot. Keep a little extra money for ACH reversals. Answer ID requests quickly. Use resources like FDIC guidance, NerdWallet, and Bankrate to compare accounts.

When comparing free online checking accounts for business, have your documents ready. Pick an account that matches your business’s needs and growth plans.

FAQ

Can you open a business bank account without a deposit?

Yes, you can open a business bank account without deposit or no deposit required upfront by choosing the bank who offer that kind of account such as Novo, Blue Vine.

Who offers free business checking accounts?

There are several banks and fintechs that offer free business checking accounts (no monthly maintenance fee or minimum balance) in the U.S. Here are a few good examples:

· FNBO Free Business Checking — unlimited transactions, no minimum balance, no monthly fee.

· Range Bank Simply Free Business Checking — no monthly service charge, no minimum balance.

· Mercury (fintech business banking) — free business checking and savings accounts, zero monthly fees.

Can an LLC get a bank account?

Yes, an LLC can open a bank account. To do so, you need to provide your LLC formation documents, Employer Identification Number (EIN), and identification for all members, such as a driver’s license or passport.